Yes, you can buy after bankruptcy.

A fresh start. A new home. FHA loans were built so that a Chapter 7 or Chapter 13 chapter in your past doesn't have to be the last one. California buyers welcome — let's see what you qualify for.

A fresh start, explained.

If you've ever wondered whether owning a home is still possible after Chapter 7 or Chapter 13 — press play. A quick, honest walk-through of what FHA actually allows.

A short note from Kiri

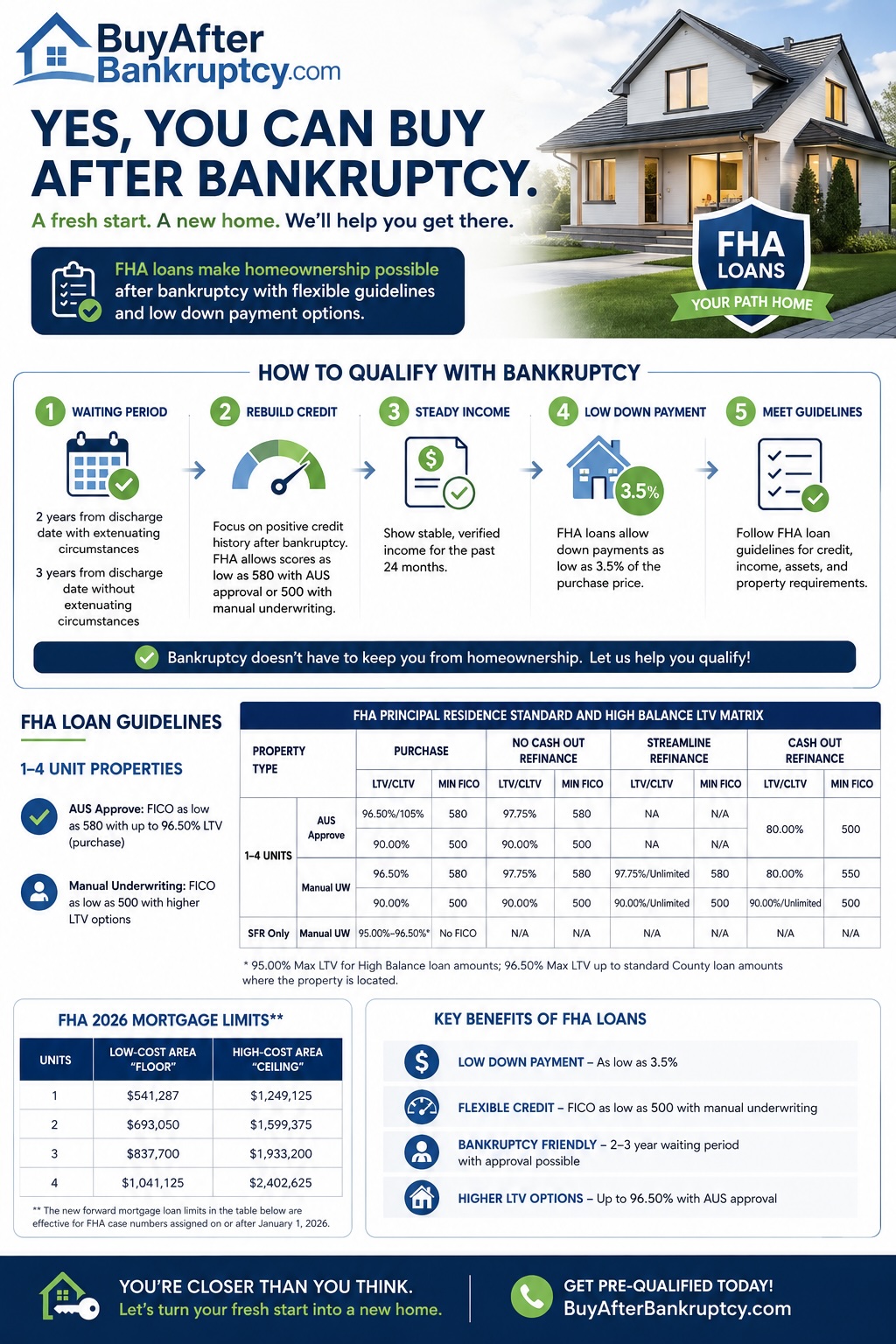

How to qualify with bankruptcy in your history.

Five focus areas that determine whether you're approvable today, or whether we need a few months to clean up the file first.

Specific FHA waiting periods after bankruptcy depend on chapter (Ch 7 vs. Ch 13), time since discharge, documented extenuating circumstances, and the individual lender's overlays. We'll calculate yours on the consult call.

FHA loan terms after bankruptcy.

FHA guidelines for owner-occupied California homes. Bankruptcy alone doesn't disqualify you — credit profile, time, and program all matter.

Source: FHA Single Family Housing Policy Handbook 4000.1 and 2026 forward mortgage limits. Not a commitment to lend.

Chapter 7 vs. Chapter 13 — different paths back.

The bankruptcy chapter you filed determines how FHA treats your file. Both chapters have a path. Tell me yours and I'll calculate the timeline.

The discharge-and-rebuild path

Filed Ch 7, debts discharged, fresh start. FHA's path back focuses on the time since discharge and the credit you've rebuilt since.

- FHA has a defined waiting period from your discharge date — we'll confirm where you land.

- Extenuating circumstances (medical event, job loss, etc.) may shorten the wait if documented.

- Post-BK credit rebuild matters: on-time payments, low balances, no new lates.

- Once eligible, full FHA terms apply — including 3.5% down at 580+ FICO.

The repayment-plan path

Filed Ch 13 and entered a repayment plan. FHA may approve you while you're still in the plan — not after, in some cases.

- Borrowers in a Ch 13 plan may qualify after a defined period of on-time plan payments.

- Written court permission to enter the mortgage is required.

- Trustee approval and plan-payment history are reviewed alongside credit.

- If your plan is complete and discharged, a separate post-discharge timeline applies.

Four steps from "is it even possible?" to keys.

You don't need a perfect file to start the conversation. The first call is honest, free, and short.

Tell me your story

BK chapter, discharge date, where your credit sits today, and what you want to buy. No judgment — I work with this every day.

Soft credit pull

With your permission. I review your actual file and lay out what FHA (and our 240+ lenders) will and won't accept right now.

Map the path back

Approvable today? We go. Need 30, 60, or 180 days to clean up a couple of items? I give you a specific list and a re-check date.

Close the loan

I route your file to the FHA lenders that actually fund post-BK files — not the ones that quote you, run your credit, then ghost.

An LO who answers honestly — even when the answer is "not yet."

"Bankruptcy isn't the end of the story. For most of my clients, it's the chapter right before they buy their next home."

I'm Kiri Suykry (legal name Kiriwath Suykry), Loan Officer at Loan Factory — 20+ years in real estate and mortgages, working in English and Cambodian / Khmer. I close FHA deals across California, including post-bankruptcy files other LOs gave up on.

Through our 240+ lender network and AI-powered platform, I match post-BK borrowers to the FHA lenders that actually fund the file — not the ones that overlay their way to a "no."

You're closer than you think.

Let's turn your fresh start into a new home.

Quick reply — usually within one business day in Pacific Time. Honest, no-pressure call. If FHA isn't right yet, I'll tell you what to fix and when to call back.

-

Call or text(949) 245-9313

-

Emailkiri@loanfactory.com

-

CoverageCalifornia property only · Loan Factory